FOR AUSTRALIANS WEIGHING UP THEIR NEXT INVESTMENT PROPERTY

The rules changed.

The opportunity didn't.

Negative gearing and capital gains tax are being reshaped, and plenty of would-be investors have gone quiet.

Here is the truth. Property is still one of the most reliable ways to build long term wealth in Australia. What has shrunk is the margin for error. From here, the investors who win are the ones who know their numbers cold before they buy.

WATCH THIS FIRST

A few minutes that could save you from a very expensive mistake.

THE HONEST PICTURE

Property still stacks up. You just have to be sharper.

The market has not closed. It has simply stopped being forgiving. Here is what actually changed, and what did not.

-

🏠 Priced out of your target suburb

Your borrowing power gets you a one-bedder 90 minutes from work. Not exactly the plan.

-

💰Stuck on the deposit

Saving 5–20% of a number that keeps growing can feel like chasing a target that won't stay still.

-

📈 Watching prices run away

Every month you wait, you need to save more. The goalpost keeps moving further.

-

⏳ Being told to wait 3-5 years

You're watching your peers build wealth while you're told to keep renting and saving.

YOUR OPTIONS

Two walls stop most first home buyers.

Here's how to get through them.

Almost every first home buyer is stuck on one of two things, sometimes both. Find yours below, then book a free call to find out exactly which strategy fits your numbers.

-

💰 Wall 1: The Deposit

Saving 5-20% of a number that keeps growing can feel impossible.

5% Deposit Scheme

A government-backed scheme that lets eligible first home buyers in with just a 5% deposit and skip Lenders Mortgage Insurance. Property price caps apply depending on location.

Guarantor Loan

Use a family member's existing property equity as security instead of a cash deposit. Can mean borrowing up to 100% of the purchase price plus costs.

Paying LMI Strategically

Sometimes paying Lenders Mortgage Insurance to get in sooner beats waiting years to avoid it, especially in a rising market. Certain professions can also access LMI waivers.

-

📊 Wall 2: Borrowing Capacity

Your deposit's fine, but the bank won't lend you enough for where you want to live.

Rentvesting

Buy an investment property while you keep renting somewhere affordable or stay living with family. Future rental income can lift what lenders are willing to offer you.

Buy With a Friend or Family Member

Combine two incomes to boost your borrowing power. Many lenders let you split the loan into separate portions, so you're only responsible for your own share.

Boost Your Income

A pay rise, upskilling, second job, or a smarter savings strategy can move the needle, especially when combined with one of the other options here.

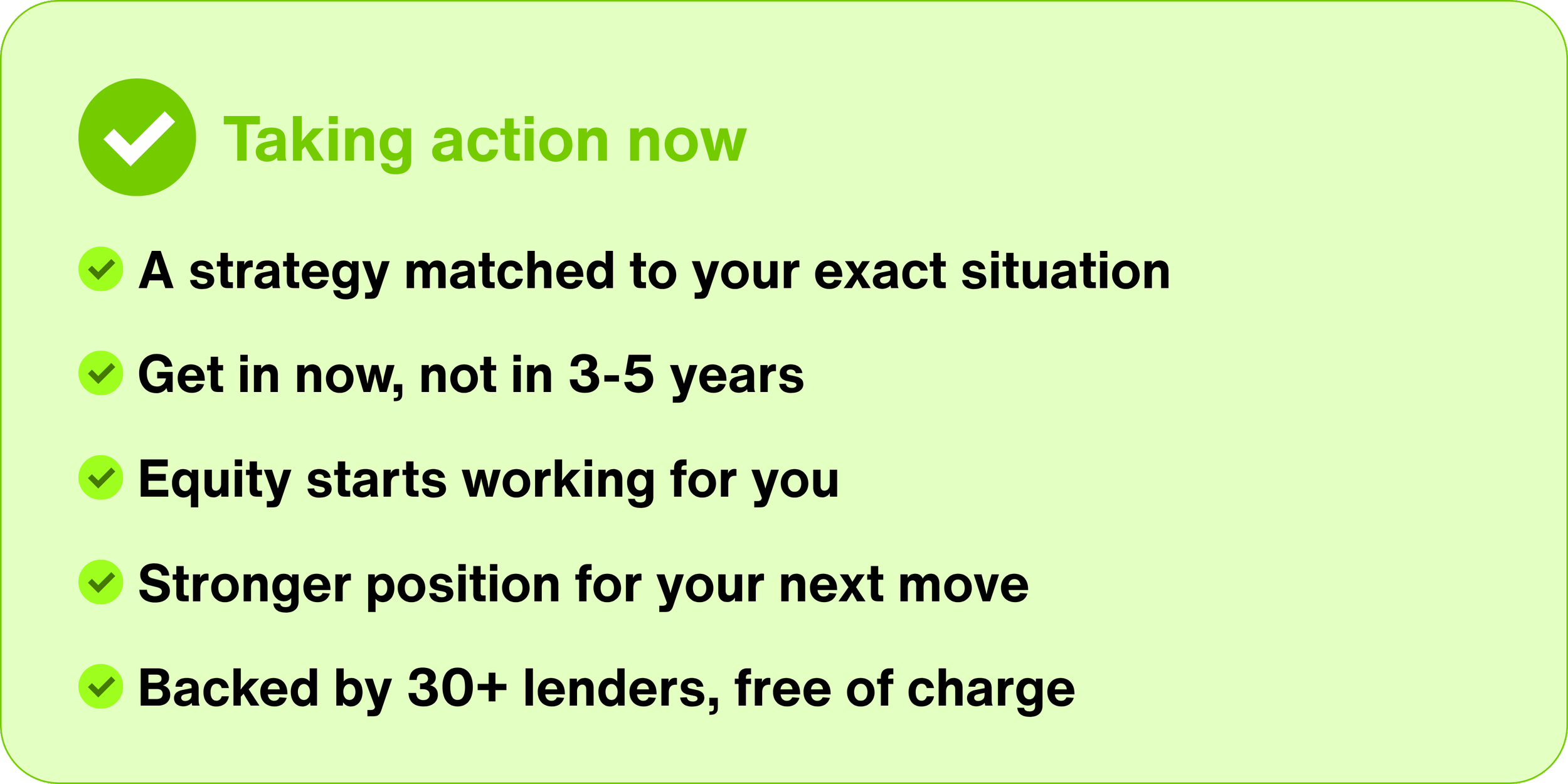

🔑 Most of our clients use a combination of these tailored to their exact numbers. That's exactly what we map out together on your free strategy call

IS THIS FOR ME?

This works if you can tick most of these boxes

You don't need to tick every single one, that's what our strategy call is for.

THE COMPARISON

What waiting actually costs you

CLIENT RESULTS

Here’s What Our Clients Say!

150+ five-star Google reviews. Here are a few of the stories behind them.

GET STARTED

See where you actually stand

Tell us a little about your situation and we'll confirm you're a good fit before we chat.

Takes 60 seconds. No obligation.

Your details are kept private. We'll never share them with third parties.

COMMON QUESTIONS

You probably want to know...

-

The 5% Deposit Scheme is a government-backed program that lets eligible first home buyers in with just a 5% deposit while avoiding Lenders Mortgage Insurance, though property price caps apply. A guarantor loan lets a family member use their own property equity as security instead, which can mean borrowing up to 100% of the purchase price plus costs with no deposit at all. Which one suits you depends on your specific situation, we'll walk you through both on your free call.

-

This is one of the most common things people are unsure about, and it's exactly what we figure out together on your free strategy call. Once we know which "wall" is actually holding you back, we can show you the specific strategies that apply to your situation, rather than generic advice that may not.

-

Not at all. Buying an investment property first is just one option, and it's the right fit for some buyers and not others. If your main issue is the deposit rather than borrowing capacity, options like the 5% scheme or a guarantor loan might get you straight into your own home instead. We assess your specific numbers before recommending any path.

-

Yes, buying an investment property first means you won't access First Home Owner schemes or stamp duty concessions. That's exactly why we assess this carefully with each client. In many cases, the capital growth and rental income from the right investment property can more than make up for those upfront savings. But we'll run the numbers for your specific situation before recommending anything.

-

This is the one of the biggest concerns most people have, and it's a fair one. We only recommend this strategy when the numbers genuinely work for your cashflow. The rental income and negative gearing on the investment property offsets your costs significantly, and we'll model exactly what your weekly position looks like before you commit to anything.

-

Once we have everything in order, most clients get a pre-approval within days and formal approval shortly after finding the right property. We make the process as fast and smooth as possible and we guide you through every step so there are no surprises.

-

Zero. Absolutely nothing. As mortgage brokers, we're paid by the lender when your loan settles. You get our strategy, expertise, and service completely free and we still have access to 30+ lenders, so we're working to get you the best rate, not just any rate.

READY TO FIND OUT?

Still thinking about it?

Every month you wait, prices move.

Book a free call. Worst case, you leave with a clear picture of your options.